Why I Think Financial Advisors Are Ignoring Your Biggest Retirement Asset

Why I think financial advisors are ignoring your biggest retirement asset is something worth saying out loud, because most people never hear it until it is too late to make a real difference. If you have a million dollars or more sitting in your home and nobody on your financial team has ever talked about it as a strategic tool, that is a problem worth understanding.

This is not about blaming anyone. It is about a structural gap in how retirement planning actually works and what you can do about it.

The Asset That Never Makes It Into the Plan

For many homeowners over 62, home equity is the largest asset they own. It is bigger than the 401 (k), bigger than the brokerage account, and, in many cases, bigger than everything else combined. That is not a small thing.

But traditional financial planning was built around investable assets, meaning stocks, bonds, and cash. That is what most advisors are trained to manage, and, more importantly, what most advisors are compensated to manage. Your house is not on their platform. It does not show up in their portfolio management software. So it just sits there, completely outside the plan, while your investment accounts carry the full weight of your retirement.

The result is that financial advisors are ignoring your biggest retirement asset, not because they are bad at their jobs, but because the business model was never designed to include it.

Why the Incentive Structure Matters

Here is the honest explanation. Most financial advisors are paid based on assets under management. The more investable assets they manage for you, the more they earn. Your home equity is not an asset they manage, so there is no built-in incentive to bring it into the conversation.

This is not a conspiracy. It is just how the model works. And it means that even advisors who are sharp, experienced, and genuinely care about their clients may never ask whether your home equity could be used in a useful way in your retirement.

There is also a training gap. Home equity strategies, including reverse mortgages, were never part of the standard licensing curriculum for financial planners. Even advisors who want to explore this territory often do not know where to start.

What Staying on the Sidelines Actually Costs You

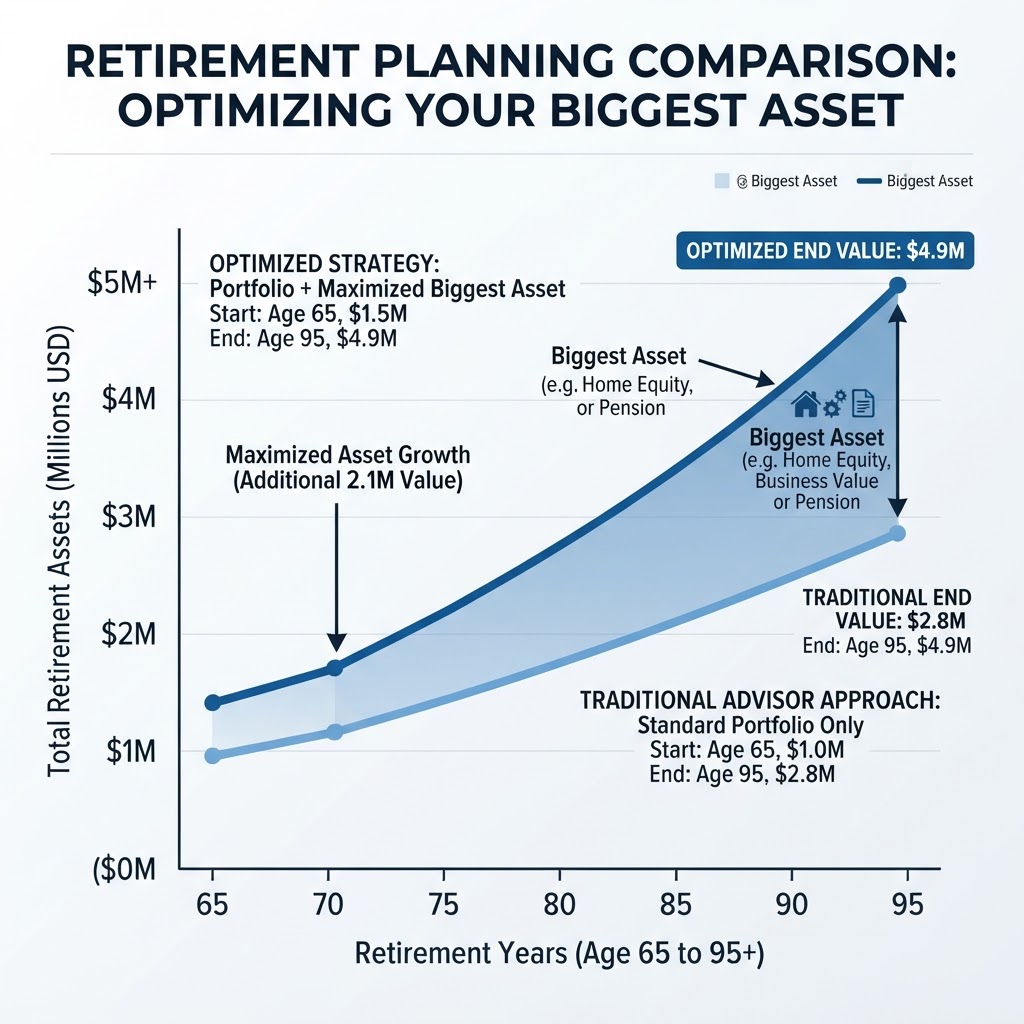

Let me make this concrete. If you are 67 years old with a million dollars in home equity, a reverse mortgage could unlock hundreds of thousands of dollars in tax-free cash or a growing line of credit, without requiring you to sell your home or make monthly mortgage payments. That is a federally insured loan product backed by the U.S. Department of Housing and Urban Development, not a fringe product or a last resort.

You can learn more about how HUD’s reverse mortgage program works directly at HUD.gov https://www.hud.gov/program_offices/housing/sfh/hecm/hecmhome.

When that equity is strategically brought into the plan, a few things can happen. You can draw down your investment portfolio more slowly, which directly affects how long your money lasts. You can reduce your taxable income in years when required minimum distributions would push you into a higher bracket. And you can use home equity as a buffer during market downturns, covering living expenses from the credit line instead of selling investments at a loss, then letting the portfolio recover before you start drawing from it again.

These are not workarounds. They are legitimate, research-backed retirement strategies that just require someone who knows how all the pieces fit together.

The Research Actually Backs This Up

This is not just my opinion. Dr. Wade Pfau, one of the most widely respected retirement income researchers in the country, has published work showing that coordinating home equity with a retirement portfolio can meaningfully extend the portfolio’s longevity. The keyword is “coordinated,” meaning you are not just randomly pulling cash from your house. You are using it in a planned, intentional way alongside your other assets.

The Consumer Financial Protection Bureau https://www.consumerfinance.gov/consumer-tools/reverse-mortgages/ also provides resources on reverse mortgages and home equity products for homeowners seeking to understand their options before making decisions.

Most financial advisors have simply never been exposed to this research in a practical, actionable way. That is the gap.

What a Coordinated Strategy Actually Looks Like

I work with clients who have used a reverse mortgage line of credit as a buffer during market downturns. When their portfolio drops, they pull from the home equity line instead of selling at a loss. The portfolio gets time to recover. The retirement income stays stable.

I have seen clients use home equity to delay Social Security, which permanently increases their monthly benefit for the rest of their lives. I have seen others reduce their tax burden in high-income years by substituting home equity draws for portfolio withdrawals.

None of this is exotic. It just requires a plan that actually includes your house.

The Question Worth Asking

If you trust your advisor and have a good relationship, that is worth protecting. This is not about second-guessing anyone. It is about asking one simple question: has anyone on your team ever looked at your home equity as a strategic tool, not just a fallback for emergencies?

If the answer is no, that is a gap worth filling.

Run Your Own Numbers

I built Perpetual Retirement to work with homeowners who have real equity and want to know if it can actually improve their retirement outlook. If you are curious what a coordinated strategy could look like for your specific situation, the first step is simple. Run your numbers yourself, no phone call required.

Run your numbers free at PerpetualRetirement.com https://www.perpetualretirement.com?utm_source=tanecabe_blog&utm_medium=blog&utm_campaign=why-i-think-financial-advisors-are-ignoring-your-b

It takes a few minutes and gives you a real starting point. If it makes sense to talk after that, I am here.