How Much Can You Actually Borrow with a Reverse Mortgage

How much can you actually borrow with a reverse mortgage? That is one of the most searched questions in this space, and it is still one of the least clearly answered. Most people go looking for a straight number and come back with vague percentages and generic disclaimers. This post is going to fix that.

Here is the short version: the amount you can access depends on a few specific factors unique to your situation. Once you understand those factors, you can get a pretty accurate estimate before you ever talk to a lender. Let us walk through exactly how it works.

The Three Things That Determine How Much You Can Borrow

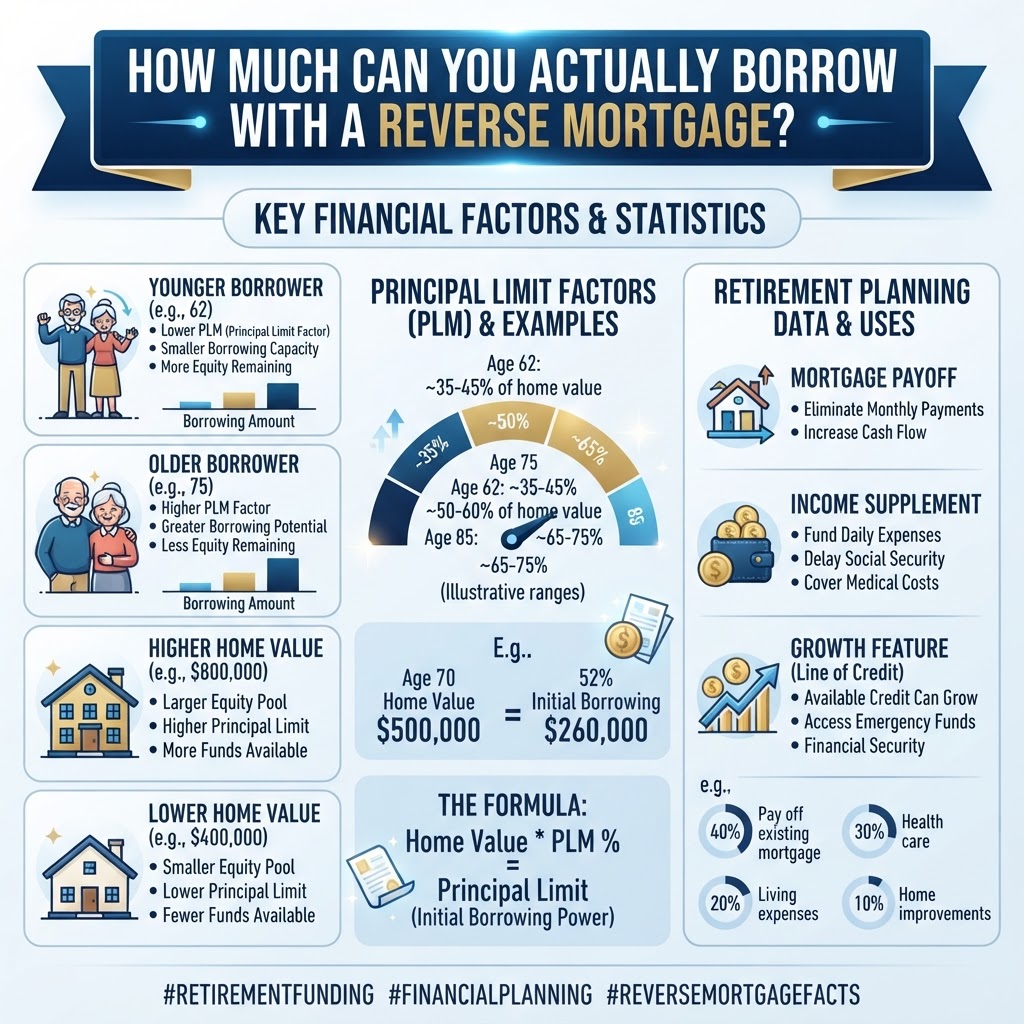

When a lender calculates your reverse mortgage, they are running three pieces of information through a formula. Your age, specifically the age of the youngest borrower on the loan. Your home’s appraised value. And current interest rates.

Those three inputs produce what is called your Principal Limit, which is just the technical term for the maximum amount you can access. The relationship is straightforward: the older you are, the higher your home value, and the lower the interest rate environment, the more money you can pull out. Age is the factor that surprises people the most, because it moves the number more than they expect.

What the FHA Lending Limit Actually Means for You

Here is where high-value homeowners often get tripped up. The FHA, the agency that backs most standard reverse mortgages, caps how much home value it will count in the calculation. As of 2024, that cap sits at $1,149,825.

So if your home is worth two million dollars, the formula does not use two million. It uses the capped amount. That means a significant portion of your equity is entirely outside the calculation.

This is one of the main reasons homeowners with higher-value properties look at a jumbo reverse mortgage instead. Jumbo products are not FHA-insured, so they do not carry that same ceiling. They can unlock considerably more equity for the right borrower. You can learn more about how FHA reverse mortgage limits are set by visiting https://www.hud.gov, which publishes current lending limits and program guidelines.

Real Numbers: What Percentage Do You Actually Get?

When people ask how much you can actually borrow with a reverse mortgage, what they really want is a concrete example. Here is a realistic range based on typical scenarios.

If you are 62, the minimum qualifying age, and your home is worth $1 million, you might be able to access $400,000 to $500,000. If you are 75 with the same home value, that number could move up to $550,000 or $600,000. Age genuinely moves the needle here, and it is one reason why waiting does not always work in your favor. Interest rates and home values both fluctuate, and neither is guaranteed to improve your number over time.

These are estimates, not guarantees. The only way to know your actual number is to run your specific age, home value, and today’s rates through a real calculation.

If You Still Have a Mortgage, Here Is What Changes

A lot of people forget to factor this in. If you have an existing mortgage on your home, that balance gets paid off first from your reverse mortgage proceeds. So if your calculation shows $500,000 available but you still owe $200,000, your net usable cash drops to $300,000.

That said, eliminating a monthly mortgage payment is often the biggest financial relief people feel after closing on a reverse mortgage. That payment is gone. Permanently. For many borrowers, even after paying off an existing loan, their monthly cash flow position improves dramatically because a major fixed expense disappears from the budget.

How You Can Actually Receive the Money

Once you know your number, you have options on how to take it. You can take a lump sum upfront. You can set up monthly payments that come in like a paycheck. You can open a line of credit that sits available and grows over time. Or you can combine those in whatever way fits your situation.

The line-of-credit option is the most underrated feature of this entire product. The unused portion of your credit line grows at the same rate as your loan interest. That means the longer you leave it untouched, the larger it gets. It is a built-in growth mechanism that most people have never heard of before they sit down and actually look at the numbers.

What About Owing More Than the Home Is Worth?

This concern comes up in almost every conversation. Nobody wants to borrow against their home and leave their heirs holding a bill that exceeds the property’s value.

With an FHA-insured reverse mortgage, a non-recourse clause is built into the loan. That means you and your heirs will never owe more than the home’s value at the time of sale. If the loan balance ever exceeds the home’s value, the government-backed insurance covers the difference. That risk does not fall on your family. The [Consumer Financial Protection Bureau](https://www.consumerfinance.gov) has a straightforward breakdown of reverse mortgage protections worth reading if you want to go deeper on this topic.

Run Your Own Numbers Before You Do Anything Else

How much can you actually borrow with a reverse mortgage? The honest answer is that the number is yours alone. It depends on your age, your home, and today’s rate environment, and nobody can give you a meaningful answer without running your actual information.

If you want to know where you stand without sitting through a sales pitch, I have a free calculator and a team that can walk you through your specific situation. No pressure, no obligation, just real numbers so you can make an informed decision. Run your numbers free at PerpetualRetirement.com https://www.perpetualretirement.com?utm_source=tanecabe_blog&utm_medium=blog&utm_campaign=how-much-can-you-actually-borrow-with-a-reverse-mo.

—

Tane Cabe is a reverse mortgage specialist at Barrett Financial and the founder of Perpetual Retirement, a resource for homeowners 55+ and independent financial advisors navigating home equity strategies in retirement.