A Rancho Santa Fe couple with a $6.9M home and a 13% chance of making it through retirement without running out of money walked into my office. They left with an 89% probability of success and 17 additional years of financial runway. They didn’t sell their home, didn’t cut their spending, and didn’t change their lifestyle. They just stopped leaving millions of dollars in home equity completely out of their retirement plan.

Here’s exactly what happened.

What the Numbers Looked Like Before

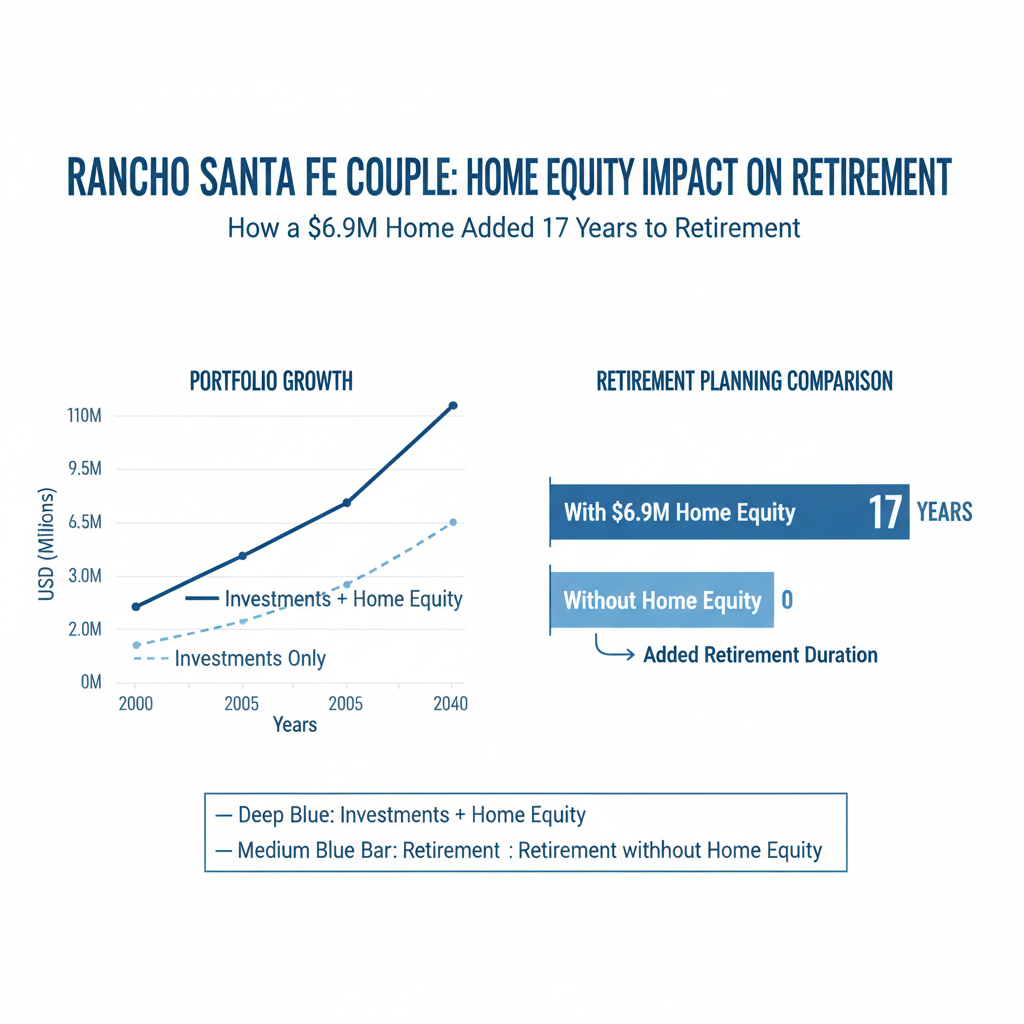

When this couple first came to me, they were 65 years old, freshly retired, and living in a $6.9 million home in Rancho Santa Fe. On paper, they looked fine. In reality, when we ran their plan through retirement-planning software, their portfolio would be down to zero by the time they turned 78.

That’s 13 years short of a full retirement.

Here’s what their situation actually looked like:

- $3,700 per month coming in from Social Security

- $400,000 mortgage balance with $3,200 per month going out the door

- $18,000 per month in total spending needs

Every single month, they were pulling heavily from their investment portfolio just to cover that gap. The stress test came back at 13% probability of success. That means there was an 87% chance they would run out of money before one of them passed away.

The painful part? They were sitting on millions of dollars in home equity the entire time. It wasn’t generating income. It wasn’t protecting their portfolio. It was just locked up in the house’s walls and foundation, completely disconnected from their financial plan.

The Move That Changed Everything

The tool we used was a jumbo reverse mortgage. This is a reverse mortgage designed specifically for high-value homes, and it lets you access your home equity without selling, making monthly mortgage payments, or giving up ownership.

For this Rancho Santa Fe couple, the total jumbo reverse mortgage amount they qualified for came to $2,911,800. Here’s how that broke down.

Step One: Pay Off the Existing Mortgage

The first thing we did was pay off the $400,000 mortgage balance entirely. Gone. That immediately freed up $3,200 every single month that was no longer leaving their account.

Step Two: Add a Liquidity Cushion

At closing, they received $327,950 in cash, which went straight into their investment portfolio. That cushion matters more than most people realize.

Step Three: Set Up the Line of Credit

The remaining $2,183,850 became a growing line of credit that they can draw from strategically over the course of retirement. This is where the real planning happens. That line of credit grows over time, meaning the longer they wait to use it, the more it’s worth.

What the Numbers Looked Like After

Before activating the home equity, their portfolio was set to go to zero at age 78. After making this move, their money, including strategic draws from the reverse mortgage line of credit, lasts until age 95.

That’s 17 additional years of financial security for this Rancho Santa Fe couple, thanks to a single planning decision.

Probability of success: 13% to 89%.

Same couple. Same home. Same lifestyle.

Why the Line of Credit Changes the Math

The reverse mortgage line of credit works as what researchers call a buffer asset. According to research published by financial planning academics and cited by organizations such as https://www.aarp.org/money/reverse-mortgages/, using home equity strategically alongside an investment portfolio can significantly improve retirement outcomes compared to treating it as a last resort.

When markets are down, you draw from the line of credit instead of selling investments at a loss. When markets recover, you let the portfolio grow. You’re giving your investments time to breathe without being forced to liquidate at the worst possible moment.

This is not a product for people who are struggling. This couple was not struggling. This is a planning tool for people who have significant equity in high-value homes and want to ensure the asset is working within their retirement strategy.

The Misconception That Keeps People from Using This

I hear this all the time: “If I get a reverse mortgage, the bank is going to take my house.”

That’s not how this works.

You remain on title as the owner of your home for the entire life of the loan. A reverse mortgage is a loan against your equity, the same concept as any other mortgage. Your heirs can still inherit the home. They simply pay off the loan balance when the time comes, and in most cases, there is still significant equity remaining.

The Consumer Financial Protection Bureau (CFPB) https://www.cfpb.gov/consumer-tools/reverse-mortgages/ has published clear guidance on how reverse mortgages work, including borrower protections and what happens to the home when the loan becomes due. It’s worth reading if you want the full picture before any conversation.

How to Know If This Applies to Your Situation

Every situation is different. The only way to know what’s actually possible for you is to look at your specific home value, your mortgage balance, your monthly spending needs, and your portfolio. There’s no guessing involved. The numbers either work or they don’t, and you deserve to know which.

If you’re 55 or older and you own a home worth $1 million or more, this conversation is worth having. I work with homeowners in Rancho Santa Fe, across San Diego, and throughout the country, and I do this analysis every day.

You can run your own numbers for free at PerpetualRetirement.com https://www.perpetualretirement.com?utm_source=tanecabe_blog&utm_medium=blog&utm_campaign=how-a-69m-home-added-17-years-to-retirement-for-a-rancho-santa-fe-couple. No pressure, no obligation. Just clarity on what’s actually possible for your retirement.