Reverse Mortgage Pros and Cons in 2026: What Nobody Tells You

The reverse mortgage pros and cons conversation in 2026 looks very different from what it did five or ten years ago, and most of what’s circulating online hasn’t caught up. If you’ve been reading the same recycled lists, you’re probably missing some important details that could change how you think about this tool entirely.

This isn’t a sales pitch. It’s also not a warning to run the other way. It’s an honest look at both sides so you can figure out whether this makes sense for your situation.

—

The Real Pros of a Reverse Mortgage Right Now

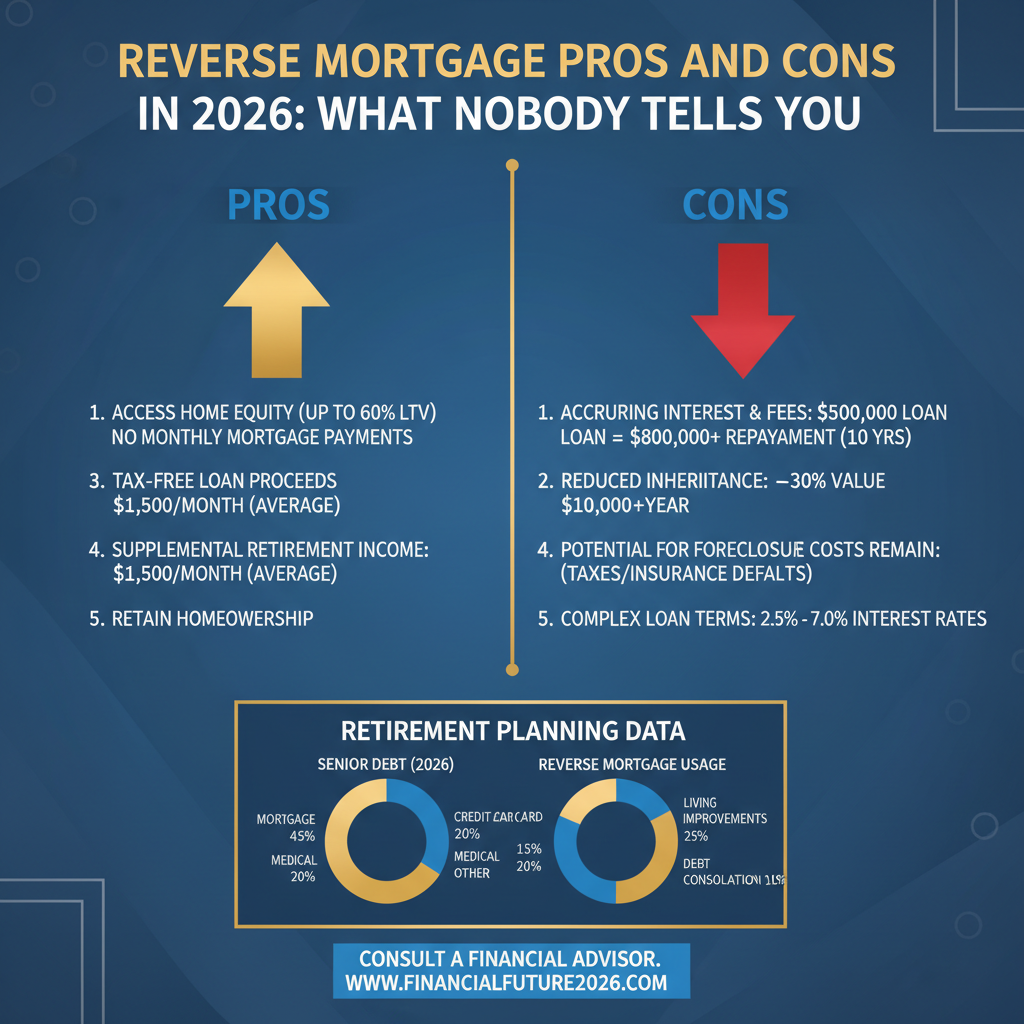

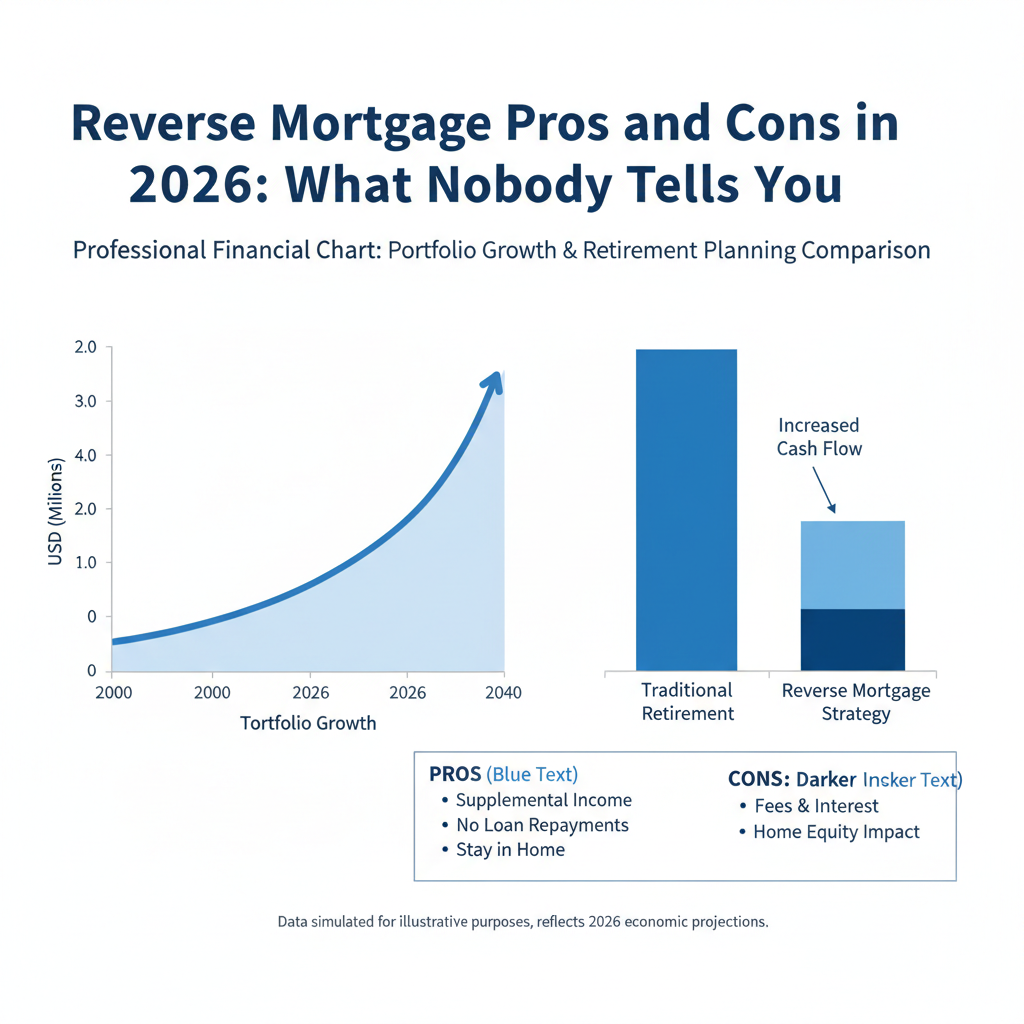

The money comes out tax-free.

When you tap your home equity through a reverse mortgage, that cash is classified as a loan advance, not income. It doesn’t show up on your tax return. It doesn’t affect your Social Security eligibility. It doesn’t touch your Medicare. For someone on a fixed retirement income, that distinction matters a lot.

No required monthly mortgage payment.

As long as you live in the home, you don’t make a monthly payment on the loan. For homeowners sitting on $1 million or more in equity, combining tax-free cash access with the elimination of a required monthly payment can completely change how a retirement budget feels and functions.

The line of credit grows.

This is the one that surprises almost everyone. If you take your reverse mortgage as a line of credit rather than a lump sum, that unused credit line grows over time. It grows at the same rate as your loan interest rate plus 0.5%. So the longer you leave it alone, the more access you have.

Set it up at 62, don’t touch it for a decade, and you could have significantly more available credit at 72 than you started with. This isn’t a marketing line. It’s how HUD has structured the product, and it’s one of the most underused retirement planning tools available to homeowners today. You can learn more about how HUD structures these loans directly at HUD’s reverse mortgage resource page (https://www.hud.gov/program_offices/housing/sfh/hecm/hecmhome).

The Real Cons, Without the Sugarcoating

Your loan balance grows every month.

Because you’re not making payments, the interest on your loan gets added to the balance each month. That balance compounds over time. If you take a large lump sum and live in the home for 20 years, the amount you owe could be substantially larger than what you originally borrowed. For homeowners who aren’t focused on leaving the property to heirs, this often isn’t a dealbreaker. But if passing the home down is important to your family, this is the real cost you need to understand before you sign anything.

Trigger events can cause the loan to come due immediately.

This is the one that catches people off guard, and it deserves your full attention. A reverse mortgage becomes due and payable when certain things happen. Those include moving out of the home, selling it, failing to pay property taxes, letting homeowner’s insurance lapse, or allowing the property to fall into serious disrepair. For most healthy, financially stable homeowners, these are manageable. But if your health changes or your finances shift, these requirements can create real pressure. Know them going in. The Consumer Financial Protection Bureau has a solid breakdown of these obligations at CFPB’s reverse mortgage guide (https://www.consumerfinance.gov/ask-cfpb/what-is-a-reverse-mortgage-en-224/).

What’s Actually Different About Reverse Mortgages in 2026

The product hasn’t changed dramatically. But the context around it has, and that changes the conversation.

Lending limits have increased. If you have a high-value home, you can access more equity now than was possible just a few years ago.

Interest rates have settled into a range that makes the line-of-credit strategy more attractive for long-term planning than it was when rates were more volatile.

Financial planners are treating this differently. More fee-only advisors are now recommending reverse mortgages as a coordinated component of retirement income planning, rather than a product of last resort. That shift in professional opinion reflects a better understanding of how housing wealth can support portfolio longevity.

What Happens to Your Heirs?

This is the concern I hear most often. People worry that taking a reverse mortgage means their kids will lose the house. Here’s the honest answer.

Your heirs can absolutely keep the home. They simply need to pay off the loan balance when you pass, either by refinancing it, selling the home, or paying it off in cash. If the home sells for more than the loan balance, your heirs keep the difference. If the home sells for less than the balance, FHA insurance covers the gap, and your family owes nothing beyond the home itself.

Is a Reverse Mortgage Right for You?

That question deserves a real answer based on your actual numbers, not a generic list. The pros and cons of reverse mortgages in 2026 vary depending on your home’s value, income, goals, and whether you have heirs who want the property.

If you want to see what this looks like specifically for your home and your situation, that’s exactly what I help people figure out. Run your numbers for free at PerpetualRetirement.com (https://PerpetualRetirement.com?utm_source=tanecabe_blog&utm_medium=blog&utm_campaign=reverse-mortgage-pros-and-cons-in-2026-what-nobody), and we can take it from there.