What happens to a reverse mortgage when you die?

What happens to a reverse mortgage when you die is one of the most searched questions in the reverse mortgage space, and for good reason. Most people assume the bank takes the house, and the kids get nothing. That is not how it works, and if that fear has been keeping you from learning more about reverse mortgages, this post will clear things up.

Let’s walk through exactly what happens, step by step, in plain English.

What Triggers Repayment on a Reverse Mortgage

A reverse mortgage becomes due when the last borrower on the loan passes away. That is the trigger. At that point, the loan balance, which includes everything you borrowed plus any interest that has accrued over the years, needs to be repaid. The keyword there is repaid, not forfeited. The bank does not walk in and take the house. Your heirs are the ones who decide what happens next, and they have real options.

This is one of the most misunderstood things about how reverse mortgages work. The lender is not waiting to swoop in the moment you are gone. There is a structured, regulated process that gives your family time to figure out what they want to do.

The Six-Month Window Your Heirs Get

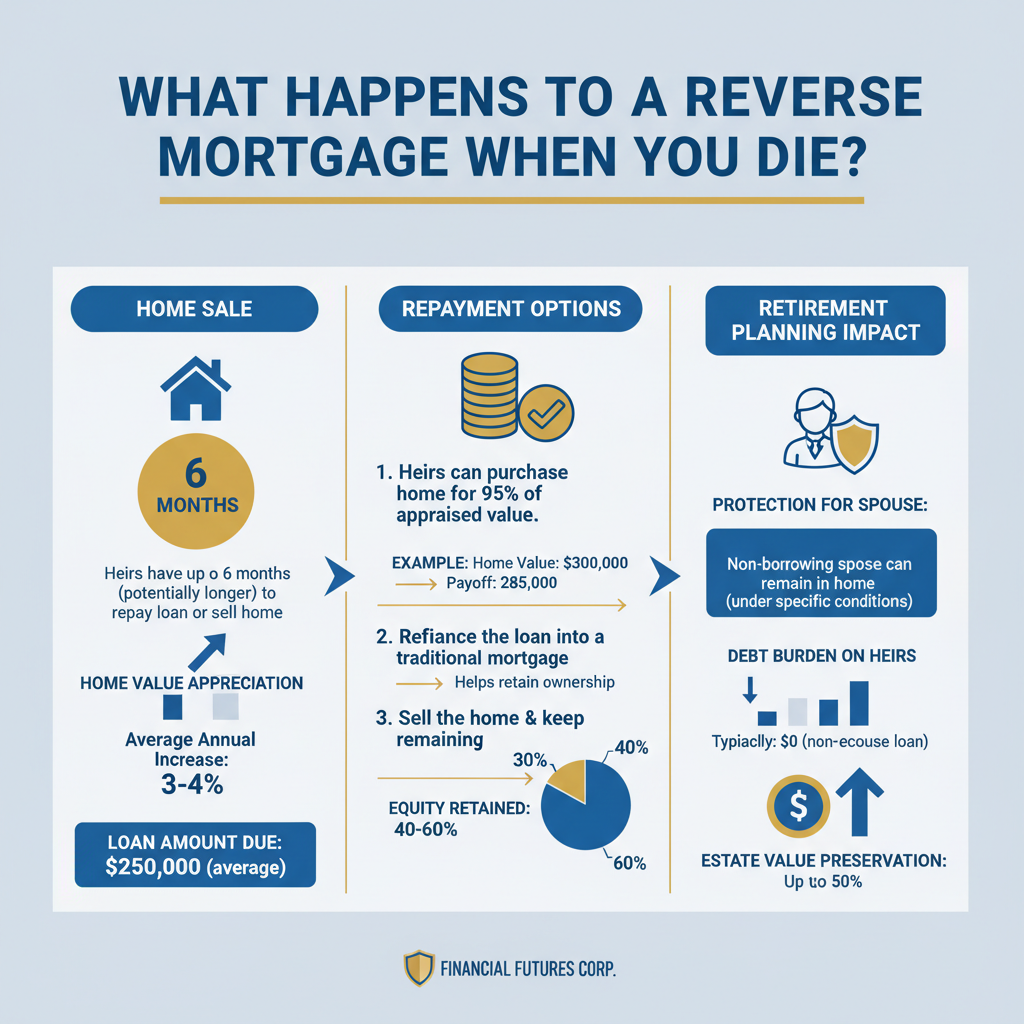

Once the lender is notified of the borrower’s passing, heirs typically have 6 months to decide how to handle the loan. That window can often be extended by up to 12 months if they are actively working toward a resolution, such as listing the home for sale or applying for a new mortgage. This is not a situation where the lender is knocking on the door the next morning.

Six to twelve months is real breathing room. Your family has time to grieve, consult with an attorney or financial advisor, and make a thoughtful decision, not a panicked one.

Two Main Options for Heirs

Option 1: Sell the Home and Keep the Equity

The most common path heirs take is selling the home. They list it at market value, sell it, pay off the reverse mortgage balance, and keep whatever equity remains. If the home is worth more than what is owed, your family keeps that difference.

For homeowners with a million dollars or more in equity, that remaining amount after years of a reverse mortgage can still be significant. The bank does not get the equity. Your family does. That is an important distinction that gets lost in the fear around these loans.

Option 2: Keep the Home by Refinancing

If your heirs want to hold onto the property, they can. They just need to pay off the reverse mortgage balance, which most people do by refinancing into a traditional mortgage in their own name. If the home is worth $1.2 million and the reverse mortgage balance is $400,000, your heir can get a conventional loan for that $400,000, pay off the reverse mortgage, and own the home free and clear of the reverse mortgage debt. This happens more often than people expect, especially with family homes that carry a lot of sentimental value.

The Non-Recourse Rule: The Protection Most People Have Never Heard Of

This is one of the most important features of a reverse mortgage, and most people have no idea it exists. It is called the non-recourse clause, and it protects your heirs in a very specific way.

If the loan balance ever ends up being higher than what the home is worth, your heirs owe nothing beyond the home itself. They can walk away. They do not have to pay the difference from their own savings or other assets. The FHA insurance that backs most reverse mortgages, formerly called a Home Equity Conversion Mortgage (HECM), covers the shortfall. Your heirs are never personally liable for a reverse mortgage debt that exceeds the home’s value.

You can read more about how HECM protections work directly from HUD’s official HECM program page https://www.hud.gov/program_offices/housing/sfh/hecm/hecmhome. The Consumer Financial Protection Bureau also has a thorough breakdown https://www.consumerfinance.gov/ask-cfpb/what-is-a-reverse-mortgage-en-224/ of reverse mortgage rules that is worth reading if you want the regulatory picture.

“But I Don’t Want to Leave My Kids With a Mess”

This is the objection I hear most often, and it is a completely understandable concern. Nobody wants to create problems for the people they love. But here is the reality: a reverse mortgage is one of the most regulated and thoroughly documented loans in the mortgage industry. The process for heirs is spelled out clearly in the loan documents. HUD has established guidelines that protect your family every step of the way, and reputable lenders will walk your heirs through the entire process.

This is not a mess. It is a process with clear rules, real timelines, and strong consumer protections built into federal law.

See What the Numbers Actually Look Like for Your Situation

If you have been hesitant to explore reverse mortgages because you were worried about what happens to your home and your family when you are gone, I hope this helped. Your heirs have options, they have time, and the law is on their side.

If you want to take this a step further and see what the actual numbers might look like for your home, including what a loan balance could look like years from now and how much equity could remain, you can run your own numbers for free at https://www.perpetualretirement.com?utm_source=tanecabe_blog&utm_medium=blog&utm_campaign=what-happens-to-a-reverse-mortgage-when-you-die. No pressure, no sales call required. Just real numbers based on your situation.